The BtR paradox: part 2

- Supply, demand, seasonality, and what these factors mean for a development’s leasing velocity.

- Seasonality on steroids: a look back at 2020.

- How do you source quality applicants, at speed and scale, regardless of fluctuating levels of supply and demand in the local area?

- A modern alternative to the expensive and obsolete traditional agency model.

In the second installment of our series on the BtR paradox, we’re going to look into supply, demand, seasonality, and how all of these factors impact the success of your lease-up efforts. The natural ebb and flow of renter demand, particularly in illiquid suburban markets, can seriously hamper a scheme’s leasing velocity without an operating model built to overcome seasonal variations. Traditional lettings agencies and in-house marketing teams, both of whom operate in a single catchment area, have no viable solution to the following problem:

How do you source quality applicants, at speed and scale, regardless of fluctuating levels of supply and demand in the local area?

While our first piece focused largely on the inefficacy of specific marketing channels and mediums common within the sector, in this article we’re going to investigate the broader structural inadequacies of traditional approaches to lease up.

Below, we explain how the best countermeasure to supply/demand seasonality is to expand the geographical scope of a single, centralised lettings operation, and why the traditional agency model is inherently ill-equipped to address the requirements of a scheme during lease up.

The Problem

Small scope, big city

As a trusted partner to many of Europe’s largest property funds, we have worked across multiple BtR schemes to lease up their developments over the past 18 months. We have therefore accumulated thousands of data points across the marketing cycle enabling us to gain a deep understanding of the number of enquiries and viewings needed to achieve the stable occupancy. Whilst several factors including seasonality, pricing, location etc., will come into play, there is a reliable formula that can be applied largely across the board.

The formula is as follows:

E/5: V/5: MI

For example, a scheme that needs to generate 250 tenancies to reach stable occupancy will require roughly 6250 enquiries and a minimum of 1250 viewings.

Operators should note that the rate at which properties are let won’t remain consistent as the weeks progress following a scheme launch. Initially, you should expect roughly one in two prospective residents to make an offer after viewing. However, as the more stubborn units remain unlet, the ratio of viewings to offers grows and the overall stats balance out around the 1 in 5 rule of thumb.

Driving this level of interest in a development is a tall order, and the approaches used in conventional lease up models are not built for success. As we discussed in our original article on the PRS paradox, neither local nor national lettings agencies have the resources required to drive demand on this scale.

This can be blamed partly on a misalignment of incentives. Lettings agents can achieve higher rates of commission by funneling quality applicants towards stock owned by private landlords (who pay higher fees) than they are likely to manage from a BtR operator. Agents also rely on punitive sole-agency contracts with their BtR clients to limit their recourse to alternative providers when they cannot deliver at the scale required to lease up a development.

It is always suspicious if an agent insists on an exclusivity clause - if their service is of a high quality then they should be confident in their ability to deliver without any concern for theoretical competition. While operators might receive discounted fees in exchange for a sole-agency contract, the agent usually stands to gain far more from such an arrangement than the client.

Even if these misalignments were eliminated, there are larger structural flaws in the traditional agency model that make it unsuitable for any scheme operator looking to lease up quickly. It simply isn’t possible to generate the volume of applicants required to fill a building if you are an agency branch that operates in one narrow area of London. This is particularly the case if you are based in a remote area of London with very little liquidity in the local market. The only way to create enough demand to lease up quickly and effectively is to source applicants from across the entire city.

It would be challenging enough to sustain bulk enquiries, even if supply and demand in local London markets remained stable and high across the year while also remaining consistent across different types of property. However, we know that this is not how markets behave. Seasonal demand varies significantly across London’s many neighbourhoods and between properties with different numbers of bedrooms.

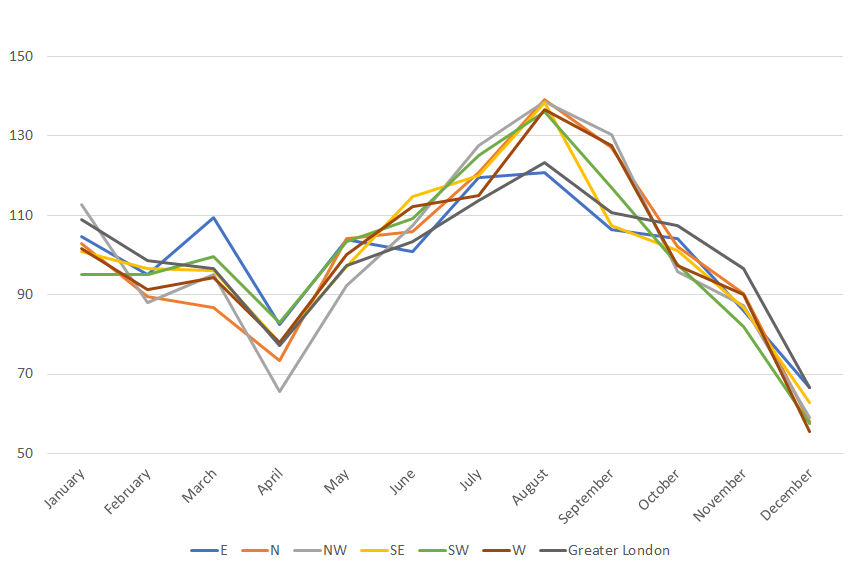

The below graph illustrates London’s indexed supply/demand stock in normal market conditions (the below represents the supply/demand average based on data from 2017-2019):

Indexed London supply/demand stock (base -100)

Supply/demand varies significantly across the year in every region of the city and, while there is a general trend towards higher demand in the summer months across every sample postcode area, not every neighbourhood experiences the exact same peaks and troughs.

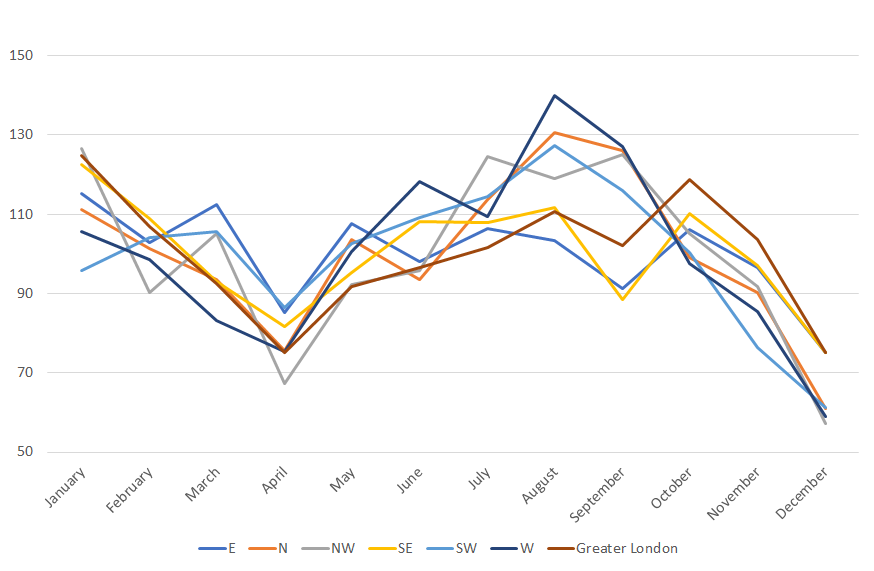

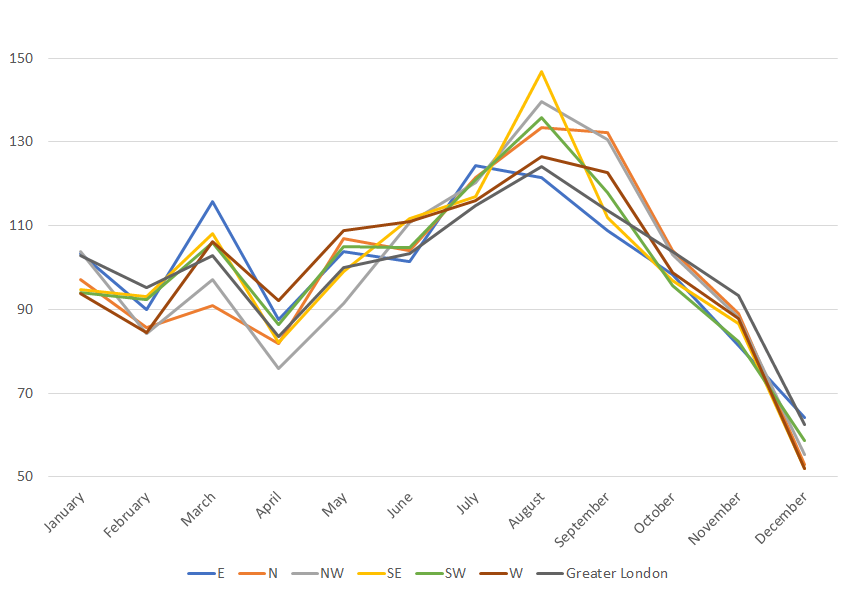

If we look at the market in granular detail, breaking down indexed supply/demand by number of bedrooms, there are even greater variations.

1 bed properties:

2 bed properties:

Demand for one bedroom properties is far less consistent across the year, both between different neighbourhoods and by comparison with two bedroom properties in the same location. For example, demand for one bedroom properties peaks in NW postcodes in July, whereas two bedroom properties in the same area receive the most interest in August. Elsewhere, demand for two bedroom properties in SE postcodes peaks higher than any other area in London, whereas one bedroom properties in the same area remains relatively modest compared with other postcodes throughout the year.

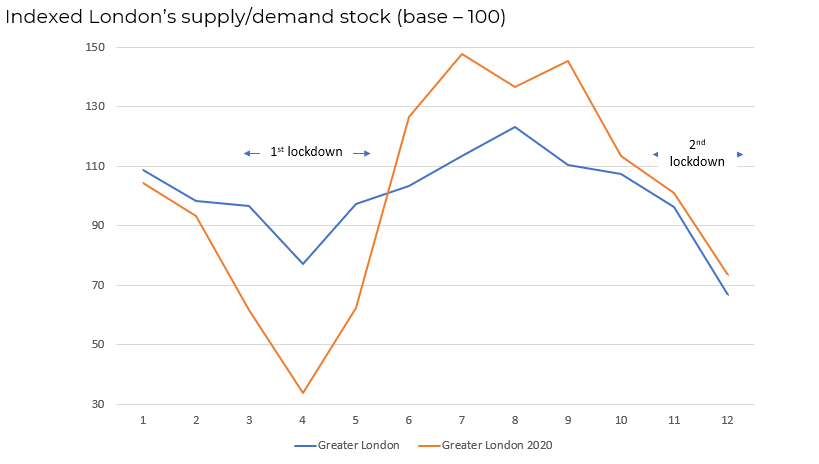

If supply and demand is subject to significant seasonal variation under normal circumstances, the external economic shock of Covid-induced lockdowns caused even wilder fluctuations:

Again, though demand recovered according to a similar general trend across London, not every postcode followed the exact same trajectory.

Local agencies operating in one narrowly defined region of the city find themselves hostage to the highs and lows of their local market throughout the year. Where organic demand for the type of units a scheme is bringing to market is low, a local agent has no access to relevant applicants enquiring on comparable properties elsewhere in the city to reach the volume needed to lease up a development.

One obvious alternative might appear to be instructing a larger national chain of agents with branches located across London. While agency chains will have access to thousands of renters across the city, the decentralised branch model inhibits larger agents from effectively serving operator needs during lease up. Individual branches operate independently and have their own targets and KPIs against which they are measured in the larger corporate entity.

In addition to the logistical challenge posed by redirecting enquiries that are not managed by a centralised administrative team, agents are not incentivised to share applicants between branches as this would mean losing out when it comes to increasing their own numbers. In practice, this means operators are unlikely to enjoy any material difference in outcomes by instructing a larger national agent compared with a local agent despite paying higher fees.

The solution

Given the structural inadequacies of both local and national agency models when it comes to leasing up a BtR development, operators must look to alternatives to ensure that top-line targets are achieved. On the basis of the problems mapped above, the only viable lease up solution is a centralised, citywide approach to lettings. This is the only model that can achieve the coverage required to consistently deliver the volume of enquiries necessary to let a building, irrespective of a scheme’s location or launch date.

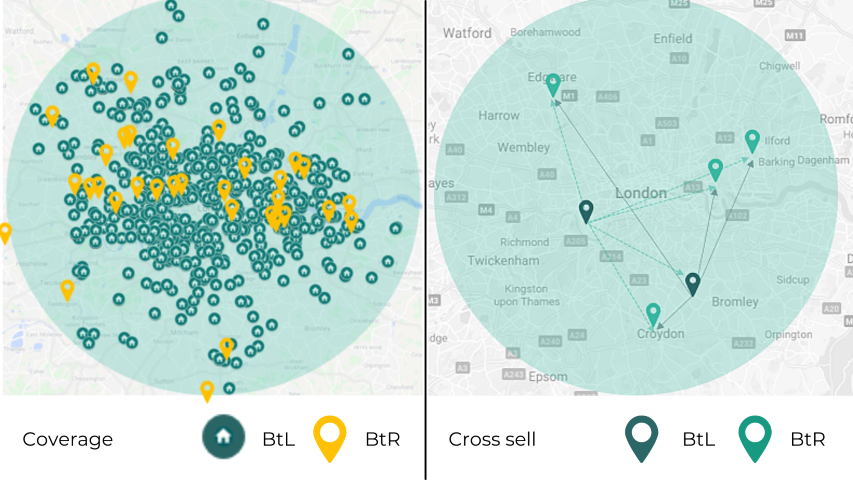

This is how we operate at Home Made. We cover the whole of London from one central location and use sophisticated, data-driven marketing methods to redirect surplus enquiries on properties across the city to various BtR schemes. Through active cross-selling, we can help operators lease up a scheme far more effectively:

Our single-branch citywide coverage, and portfolio including tens of thousands of units owned by both private and institutional landlords, allows us to access an applicant pool of sufficient size to generate thousands of unique enquiries. Nevertheless, an operator might reasonably argue that scope of coverage does not necessarily translate into an increased volume of enquiries for their development. How can you cross-sell a property in Archway to a renter looking to move to Peckham? The answer lies in our data-driven approach to property marketing.

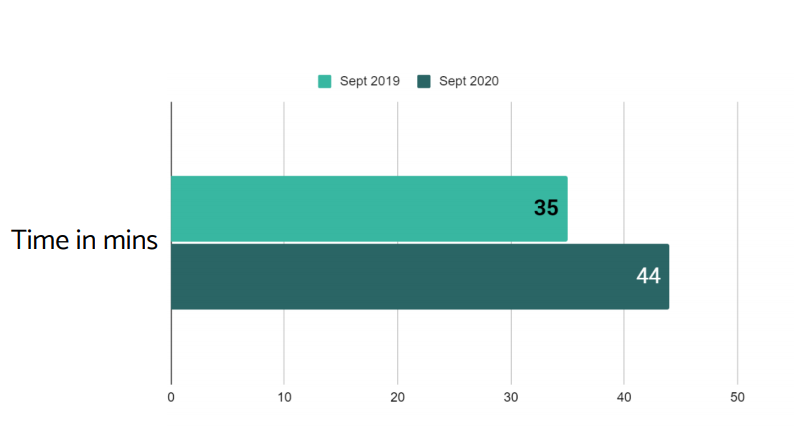

The breadth of our coverage means that we have data points from hundreds of thousands of renters enquiring on tens of thousands of property: we understand who your renters are, what they are looking for, and where they will and won’t compromise. We know that 64% of London’s renters relocate to a completely new neighbourhood when moving to a new home. The average journey time from location of origin to target property in 2020 was 44 minutes. This is an increase of \>25% compared with 2019:

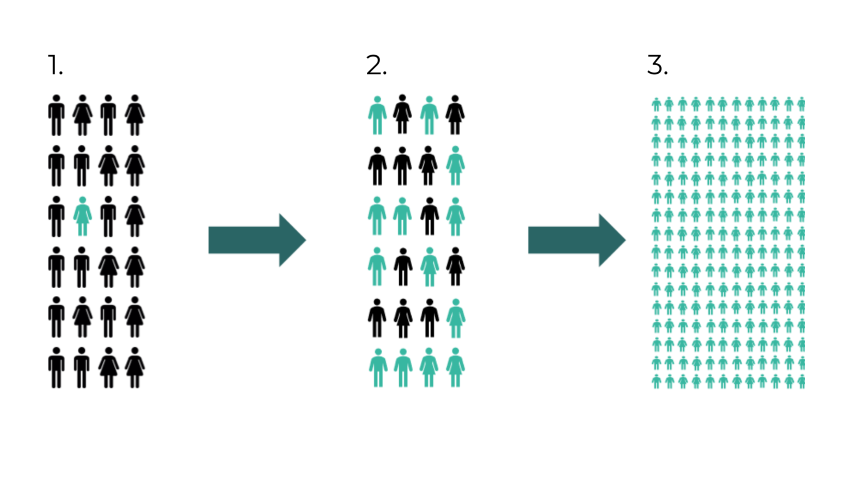

Renters are remarkably flexible when it comes to where in London they live and don’t develop a strong attachment to a particular neighbourhood. As we explained in our previous article, 30% of our property enquiries come from Londoners already logged in our database following an enquiry on a different property. By using data collected during a detailed qualification process, we pitch a range of properties outside of an applicant’s original search area. Provided the properties remain highly relevant based on their established wants and needs (e.g. outdoor space, commute time, local amenities), many renters are receptive to neighbourhoods they hadn’t previously considered.

Based on our data, we know that an average of 24 renters will apply on every private property. As each unit can only host a single tenancy, that leaves 23 pre-qualified prospective residents still searching for a new home. With our existing knowledge of their budget and search criteria, we can pitch relevant BtR units to renters in our database who did not originally search anywhere near that scheme's location. This exposes a development to thousands of additional would-be residents.

By leveraging the sheer volume of data we collect by virtue of our citywide coverage, we have developed a sophisticated marketing strategy without the constraints of local and national agents. Our fortunes are not as vulnerable to the seasonal rhythms of local London markets, and therefore neither are those of our partners.

We are, as always, here to help and if you want to speak to us about how we can support the lease-up of your scheme get in touch with Jo Green for a bespoke proposal.

Check out more of our articles here and follow us on Twitter, LinkedIn, Instagram, and Facebook for regular insights on the industry, market news, and company updates from Home Made.